Booms and Busts – 2016, by Tom Bolas - VP at International Supply Chain Solutions

"Observations from Main Street versus Wall Street"

Tom Bolas - VP at International Supply Chain Solutions20/04/2016 22:20

Q2 2016 and the “Global Economy” continues to limp along leaving catastrophic damage to countries, industries, and people. Political leaders point fingers in all directions seeking to blame others and promising solutions. Where is the light at the end of the tunnel?

I. What is the “Current” Global Economic status?

Advanced Economies (the “Demand” side of economic transactions) have been left with an overhang of Monetary Issues (Debt and damaged “Purchasing Power” of currencies) and Political/Structural Issues – (Population Aging especially Europe and Japan, Low Productivity Growth and excessive Domestic and International Regulations.

Emerging Economies (the “Supply” side of economic transactions) were left with an overhang of Monetary Issues (decreased cash with inability to Service Debt and damaged “Purchasing Power of currencies (except China which has subsequently devalued the Yuan) and Political/Structural Issues (Excess capacity and young populations (Natural Resources, Capital and Human Resources), Under-developed/Uncompetitive domestic infrastructures (Highways-transportation, factories, utilities, water supplies, agriculture, education and others), Under-developed domestic consumption (especially China, India, Russia, Middle East, Africa and Latin America), and Internationally Imposed Regulations (i.e. Climate Change).

II. What is being done to address the issues?

Monetary Issues (Debt and Currencies) – The Balance Sheets of Financial Institutions in “MOST” economies are holding “Trillions” in unsecured debt and debt in default. Contrary to “Generally Accepted Accounting Principles” they have not been forced to subject these “ASSETS” to the “Lower of Cost or Market” rules. Excluding off balance sheet liabilities, at year-end (2015) the ratio of total public and private debt relative to GDP stood at 350%, 370%, 457% and 615%, for China, the United States, the Eurocurrency zone, and Japan, respectively. Central Bankers know that to escape this debt without total economic collapse they have limited options. In all options there is a fundamental question – “How to use Inflation?” Utilized as a “Monetary Tool”, Inflation will facilitate the repayment of debt but will undermine and potentially destroy the “Purchasing Power” of the Domestic Currency. To date, Central Bankers have done little/nothing “EFFECTIVE”.

Political/Structural Reforms of Laws, Regulations, Taxes, Labor, Government Spending (i.e. Welfare, Housing, Health, Education and Military etc.) are needed to tackle structural impediments to growth in all economies. Politicians (in most economies) have either made conditions worse or have done nothing “EFFECTIVE” due to fear of losing their next election. Consequently, the paralysis in Europe, US, Japan and severe economic conditions in Brazil.

III. What can you do?

Recessions and Depressions have occurred throughout recorded history some milder and shorter some longer and more severe. The causes span every conceivable reason and “after the fact” analysis generally prove that ACTIONS taken by people, industries and countries cause RECOVERY to start and gain momentum.

To compare a few macro-economic differences between the Great Depression (1930’s) and today’s Great Recession (2009 to 2016):

• In 1930 - Financial Institutions and Corporations due to “prior mistakes” failed and were liquidated. Today – Financial Institutions and Corporations are in “worse shape” but governments have “Stepped In” and strong businesses are made to subsidize the weak extending and compounding the problems.

• In 1930 – Regulations, imposed by Governments, prolonged the Great Depression. Today – Even heavier, National and International regulations, are creating severe distortions.

• In 1930 – Taxes were generally low and most people did not pay. Today – Everyone pays and the “combined” taxes near 50%.

• In 1930 – Prices were subjected to a “Deflationary Collapse”. People who held currencies (with the exception of post WWI Germany) were positioned for subsequent success. Today – Due, to enormous Central Bank creation of monetary stimulus, prices MAY increase tremendously. People holding currencies (i.e. Euro) MAY suffer the significant loss of purchasing power. This is unknown due to the pre-recession creation of credit swaps and leverage that still exists in the economies.

• In 1930 – Economies were local and national and national legislation (Smoot-Hawley) was passed to “protect” those businesses. Today – the whole world is interdependent and tariffs have been reduced or eliminated to facilitate “Global Competition”.

What do these macro issues mean to your business? You, individually, cannot change Regulations, Taxes or Economies. You MUST address PRIOR MISTAKES and strategically prepare for Price Volatility.

Key to the “Actions” required to initiate the “Recovery” is an understanding that Boom and Bust cycles are NORMAL BUSINESS CYCLES and will occur. While we like the “Boom” cycles and detest the “Bust” cycles the problems and solutions we seek to the Busts originate in the Boom.

To define and prioritize the problems and solutions we have to look backward at the period prior to and including the BOOM. During the early phases of the Boom Cycle, OPTIMISM is growing, Government reduction of regulations, taxes and policies (properly constructed) stimulate expansion, business Growth Strategies are created, Financing is available and secured, Long Term Capital is invested, Customers are attracted and are willing to buy, Employees are hired, Vendors and Suppliers are identified and contracted to meet business needs, Technology is developed, Spending (on Capital, Direct Materials and Services, Indirect Materials and Supplies, and Infrastructure) occurs in a disciplined and conscientious manner. This is where the PRIOR MISTAKES occur but are not recognized or corrected.

When the inevitable slowdown in the economy begins the symptoms are manifested either slowly or in some cases dramatically including:

• Market demand slows, re-trenches or disappears (reducing cash),

• Inventories grow and turnover slows creating obsolescence (not creating cash),

• Cost effective goods and services alternatives, from competitors, appear to grab market share,

• Price competition starts a race to the bottom erasing margins and reducing cash flow,

• Product/Service Line profitability deteriorate leading to reductions or eliminations decreasing cash,

• Competitors declare bankruptcy due to mismanagement to protect the business from creditors,

• Internal cost structures become unsustainable (consuming cash),

• Organization structures become unsustainable (consuming cash),

• Surviving Vendors negotiate to preserve volumes,

• Employee contracts and benefits become unsustainable (consuming cash),

• Good Employees leave or are recruited by others,

• Investments in new technology are sacrificed causing stagnation in the market

• Litigation from Competitors, Customers, Employees, Vendors and Government increases (consuming cash),

• Capital Assets sit idle and depreciation accelerates

• Financing and Lines of Credit disappear or become unaffordable (reducing cash)

• Corporate Value and Stock prices collapse,

• Board of Director members resign,

• Senior Executives resign or are terminated,

• Business Strategies are abandoned.

In hindsight it is apparent that the “Business Strategies” did not include a response mechanism to economic change.

The Great Depression – 1930’s

In reviewing the business performance of mega-cap companies during the 1929-1933 period the best companies to own were diversified conglomerates (General Electric), consumer staples – (General Mills), railroads – (Union Pacific), and water utilities – (York Water). The stock prices of these companies did not hold up well during the Great Depression, but rather, that the earnings and dividend (read CASH) declines were only in the vicinity of 15-35% during the worst of the period.

One of the few companies with a business model out there that actually managed to endure the Great Depression without missing a beat was Nestle SA.

Nestlé was becoming so strong with products and technology, that it seemed even the Great Depression would have little effect on its progress. Nestlé created new subsidiaries in Argentina and Cuba. Despite the Depression, Nestlé added more production centers around the world, including a chocolate manufacturer in Copenhagen and a small factory in Moravia, Czechoslovakia, to manufacture milk food, Nescao, and evaporated milk. Factories were also opened in Chile and Mexico in the mid-1930s. While profits were down 13% in 1930 over the year before, Nestlé faced no major financial problems (read CASH) during the Depression, as its factories generally maintained their output and sales were steady.

Procter and Gamble, the consumer products company, came out of the Great Depression smelling better than it had in 1929. How did the soap giant beat the Depression? P&G realized that even in a depression people would need soap so they might as well buy it from Procter and Gamble. Thus, instead of throttling down its advertising to cut costs, the company changed strategy and actively pursued new marketing avenues, including commercial radio broadcasts. One of these tactics involved sponsoring daily radio serials aimed at homemakers, the company's core market. In 1933 P&G debuted its first serial, Oxydol's Own Ma Perkins, and women around the country quickly fell in love with the tales of the kind widow. The program was so successful that P&G started cranking out similar programs to support its other brands.

The Great Recession – 2009 to Current

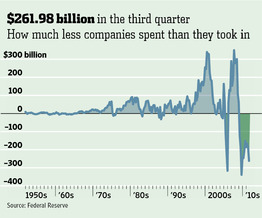

The Big Winners have been the largest U.S. corporations. It reflects the fact that they were in a position to use the recession as a positive opportunity to restructure and become more efficient. Organizations that had the resources (read CASH) to see the future and position themselves accordingly have typically been the largest corporations. Most have been able to take advantage of reduced labor costs and low interest rates to boost their productivity at the same time that they are strengthening their balance sheets.

Top companies are able to refinance their Debt (preserving CASH) at low interest rates offered by The Federal Reserve’s policy of quantitative easing at low interest rates. As a result, the value of corporate balance sheets has risen by 28% since late 2009. Corporate cash holdings (Q3-2011) were immense. Nonfinancial Companies were taking in hundreds of billions of dollars (CASH) more than they needed to fund operations.

Total cash reserves at U.S. corporations in 2015 total more than $2 trillion, close to a 50-year high in relative terms. Perhaps not surprisingly, some of the companies with lots more cash on hand than they need are paying ample dividends.

• Oil giant Chevron, with $20 billion in cash, offers a 3.1% yield.

• Chipmaker Intel, with $15 billion in cash, pays 3.3%. and

• Health-care conglomerate Johnson & Johnson, with $30 billion in cash, yields 3.5%.

Technology companies which historically paid no or very low dividends include:

• Microsoft with $102.3 billion in cash, offers a 2.58% dividend,

• Google/Alphabet with $71.9 billion in cash, with NO dividend, and

• Apple with $41.6 billion in cash, with 1.86% dividend and holding cash offshore.

In part, these huge cash reserves reflect the uncertainty corporate executives feel about whether to expand right now. Demand is still soft, government policy on taxes and regulations is confused, and risks of a currency collapse in Europe are impossible to gauge. As a result, many U.S. companies are simply hunkering down and hanging onto their money until the picture gets clearer.

IV. The “Constant of Change” is happening in the face of Economic Challenges.

Changes in the Global Economic “Infrastructure” have also undermined recovery actions as OIL prices collapsed under reduced demand (caused by excess supply and alternative energy systems, solar and natural gas discoveries) and transitions away from traditional energy (COAL). Increased employment of technologies at the personal and business levels. Wars in the Middle East. In Europe, Japan and the U.S. economic priorities have changed due to aging populations away from growth and consumption toward sustaining the existing infrastructures and reduced consumption.

Response to Changes to the Global Infrastructure can be viewed as a problem or an opportunity for innovation. Those viewing it as an “Opportunity” (and have taken Actions) include companies like:

• SCHLUMBERGER and HALLIBURTON – Fracking,

• AMAZON - Superior technology in Logistics and Distribution Systems,

• HONDA - Robotics,

• NETFLIX - Entertainment via the internet

• 3D SYSTEMS 3D Print manufacturing of custom medical solutions

• TESLA - “Electric” automobiles

• APPLE - IPhones and computer tablets

TO SUMMARIZE - the “ACTIONS” that have been taken “By Companies and People” have emphasized CASH preservation strategies and cost reductions from the prior mistakes or excesses that occurred during the BOOM years and in some cases innovation.

The ACTIONS involved SURVIVAL of the enterprise reducing costs and preserving cash and credit. These actions require the hard decisions on:

• Honest Supply-Demand Management in response to markets,

• Improved knowledge of Markets, Costs, Profits and Competition,

• COMPREHENSIVE COST REDUCTIONS and significant outsourcing,

• Exploiting the power and potential of the TOTAL Supply Chain (the extended enterprise),

• Sustainment of viable R&D-Innovation,

• Divestment of Non-performing assets and employees,

• Re-Financing of Long Term and Short Term Debt,

• Organizational Change (Board, Officers, Managers, and Employees) and

• Revised Corporate Strategy

Going forward companies are positioning their resources (Capital and Human) to respond to both Financial Changes (driven by Central Banks) and Political/Structural Changes (driven by Politicians) while preserving cash and financing for the next Boom.

Petrobras reaches net income of R$ 32.7 billion in the t...

07/11/25IBP Advocates Global Criteria for a Just Energy Transition

07/11/25Decommissioning Takes Center Stage

07/11/25ANP Approves Action Plan on Gas Pipeline Transportation ...

07/11/25AI is no longer a side project: Technology leaders at AD...

05/11/25ANP Holds Workshop on Methane Emissions in Partnership w...

05/11/25International Energy Event Opens Registration for Activities

05/11/25Norway and Brazil Launch New Joint Research Funding Call...

05/11/25DeepOcean and Jana Marine enter Saudi Arabia subsea part...

04/11/25ADIPEC 2025: Industry calls for policy pragmatism, embra...

04/11/25Johnson Matthey: Leadership and Innovation Driving the G...

31/10/25OTC Brazil connects the Equatorial Margin’s potential to...

30/10/25New Version of ANP’s Greenhouse Gas Emissions Dynamic Da...

30/10/25Port of Açu and IKM Advance Partnership to Create Brazil...

30/10/25Port of Açu and SISTAC Sign Agreement to Provide Decommi...

29/10/25Royalties from August Production Distributed to States a...

29/10/25