A new threat to the Brazilian oil and gas industry, by Telmo Ghiorzi¹

Telmo Ghiorzi

04/04/2017 19:26

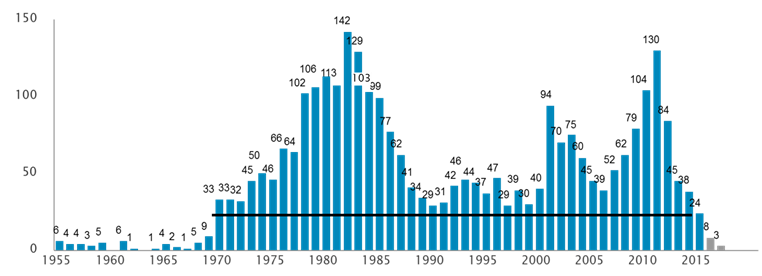

The Brazilian oil and gas industry faces a drastic reduction in its activity. Among several indicators of this, one to be highlighted is the reduction in the number of wells drilled per year. Drilling is the activity the paves the following activities in this industry and, therefore, its reduction implies reduction to the whole sector. A study performed by ABESPetro and Accenture, based on data from the Brazilian Agency of Petroleum (ANP), indicates that the number of wells drilled in 2015 and 2016 can only be compared with data from 1969. The figure below shows the evolution of this indicator.

Fig. 1 – Number of drilled wells per year (source: ABESPetro/Accenture)

The oil and gas sector is characterized by fluctuations caused by variations of the oil price, by the inherent cycle of exploration-development-production-deactivation and by the natural changes in the behavior of the reservoirs.

In Brazil, however, one testifies variations even more intense than those of the international scenario. The country is facing what some analysts call the “perfect storm” of the Brazilian oil and gas industry. The combined effect of low oil prices with the decrease of Petrobras activity because of the so-called “Lava-Jato” scandal.

Brazilian Government has announced new bid rounds to be realized in 2017 and more predictability regarding following years. This has created positive expectations to the sector, in particular to oil companies operating in Brazil and to the system of suppliers.

However, there is an element that remains as a “Sword of Damocles” over the Brazilian oil and gas industry. No matter how positive the local initiatives are, they cannot resist the threat of the shale oil. The innovation introduced by the USA in the production of hydrocarbons considered inaccessible years ago brought two challenges to the Brazilian oil and gas sector. One is general. Many analysts converge that the shale is replacing OPEC in the most influencing factor of the oil price dynamics. This new source of oil brought the dynamic of low for longer. The world may have oil prices around US$50-70/bbl for many years to come.

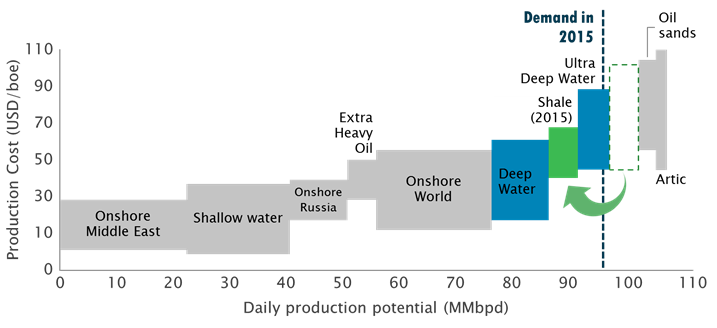

There is another threat that may hit specifically and directly the Brazilian oil and gas industry. The shale oil, since 2015, has displaced the oil produced in ultra-deep-waters (UDW). The innovation of the shale oil production was followed by other innovations that reduced its production costs to levels below the production cost from UDW. The figure below shows this effect.

Fig. 2 – Displacement of UDW oil by the shale oil (source: ABESPetro/Accenture)

The figure indicates that additional demand of oil will be preferably supplied by shale oil rather than oil from UDW. In other words, the shale oil development may imply, in the limit, that the Brazilian pre-salt will not see its potential turned into real economic benefits.

The way the shale oil industry evolved, based on the innovation competence present in the USA in general and, in particular, in its oil and gas industry, must be applied to Brazil. Innovations must be introduced to allow continuous improvement of the pre-salt competitiveness. There is no doubt of the technical feasibility to explore the pre-salt. The question arising now is on the economic feasibility of exploring the Brazilian pre-salt. And the answer is in the innovations, incremental or disruptive, that will improve the pre-salt competitiveness.

What defines the economic phenomenon ‘innovation’ is the commercial success of an idea or invention introduced in the market. The essence of the Capitalist system is this permanent creative-destruction cycle. The Brazilian oil and gas industry needs innovations to ensure its robustness and competitiveness in front of the shale oil threat.

Innovations and competence to innovate result from a combination of several factors. Public policies are important ones among them. In Brazil, there are two public policies that are of particular criticality to stimulate innovation in the petroleum industry. They materialize in the regulations of Local Content (LC) and of Research, Development and Innovation (RDI).

The CL is been reviewed. Reduction in LC requirements and process simplification are positive changes. Improvements in the direction of stimulating capability and innovation instead of focus in capacity would also be beneficial. The PEDEFOR decree (signed in 2016, not yet implemented), by recognizing and awarding with extra CL the local design and engineering of products, goes in this direction. Engineering is one of the key-activity to induce innovations. It is, therefore, an essential factor in the construction of economic feasibility of any industrial sector.

The RDI regulation can also be improved in the direction of actually stimulating innovation. Innovation is strongly dependent on the interaction of the different industry actors, such as oil companies, suppliers and universities. The impressive success cases resulting from these interactions in USA and in Europe do not repeat in Brazil. An RDI regulation that promotes this interaction, while stimulates key-activities to induce innovation such as engineering, is essential to create and keep the economic feasibility of the Brazilian oil and gas industry.

The threat of the shale oil made it clear an impasse to the Brazilian petroleum industry. All ingredients of a successful development are present, since the country has the largest UDW oil reserves of the world, many oil companies with local operation, a mature system of suppliers and universities with recognized competence to produce science and technology. However, its regulatory framework is not effective when it comes to development of innovations and, therefore, to ensure its economic feasibility. This framework must be reviewed to turn the oil from UDW into economically feasible resources. In such quest for feasibility, one can seek turn Brazil into a global reference in technology and capability to explore petroleum from UDW.

[1] Telmo Ghiorzi, MSc in Petroleum Engineering and PhD in Public Policies, is board member of the Brazilian Association of Suppliers of Goods and Services to the Oil Industry (ABESPetro – www.abespetro.org.br)

Museum of Petroleum and New Energies will operate in the...

19/03/26Macaé Energy: debates focus on the strategic role of nat...

18/03/26Macaé Energy 2026 strengthens the municipality’s positio...

17/03/26With record-breaking attendance, the Macaé Energy trade ...

17/03/26Trendsetter Vulcan Offshore Customizes Tethered BOP Tech...

17/03/26FIRJAN: Technical Conference is a Highlight of Macaé Ene...

16/03/26Inclusion of 15 New Blocks in Permanent Offer (OPP) Bid ...

14/03/26Rio City Hall Signs Agreement to Transfer Automóvel Club...

13/03/26Porto do Açu Sets Historic Record in Cargo Handling

13/03/26Following COP30, IBP Organizes Meeting to Debate Brazil'...

13/03/26Resolution Approved to Revise Aviation Kerosene Quality ...

13/03/26ANP to Participate in Research Project on Increasing Bio...

13/03/26Petrobras Paid R$ 277.6 Billion in Taxes and Government ...

13/03/26Two new discoveries in the North Sea

11/03/26At Macaé Energy 2026, FIRJAN Promotes Special Edition of...

09/03/26Innovation, ESG, and Sustainability

06/03/26Artificial Intelligence drives increased demand for elec...

02/03/26Despite Tariff Hikes, Oil Drives Rio's Trade Flow Up 9% ...

27/02/26December Production Royalty Payments Distributed to Stat...

26/02/26BRAVA Energia Wins Top Honor at OTC Houston for Atlanta ...

26/02/26ABPIP Presents 2026 Strategic Agenda to Chairman of the ...

26/02/26